Intéressé ? Contactez-nous maintenant

Pour nous contacter, veuillez remplir le formulaire à droite ou nous envoyer directement un email à l'adresse ci-dessous

sales@senecaesg.com

This June 13th, the European Commission has brought forward a new set of proposals designed to impose stricter regulations on ESG rating agencies to protect and strengthen sustainable investing. Within the proposal, changes to the way ESG rating agencies offer their services to investors and companies in the EU will allow for better-informed decision-making regarding sustainable investments.

Currently, ESG ratings and data are used by investors to evaluate the environmental, social, and governance (ESG) performance of companies. However, there are several shortcomings which market regulators, companies, investors, and NGOs have raised their concerns on:

Among many, key criticisms include:

European Commission response

Within the new draft legislation proposed by the Commission, certain obligations are being imposed to address several of these concerns. These obligations include discontinuing the provision of consulting services to investors, ceasing the sale of credit ratings, and refraining from developing benchmarks.

To ensure compliance, ESG rating agencies will need to be authorized and supervised by the European Securities and Markets Authority (ESMA). The consequence of not doing so could lead to a hefty fine amounting to about 10% of the entities’ annual net turnover.

While both the IOSCO and ESMA have been actively involved in efforts to promote reform and call for tighter regulation they have faced criticism for not acting sooner and presenting their recommendations to securities markets regulators and ESG ratings agencies. In their 2021 ESG Ratings and Data Products Providers report, IOSCO highlights several key issues. These include a lack of clarity and alignment on definitions, insufficient transparency regarding methodologies used, uneven coverage of products offered, potential conflicts of interest, and the need for improved communication with companies being rated.

While in ESMA’s 2022 report, a lack of standardization among rating agencies was highlighted. ESMA noted the increasing number of users of ESG ratings often engage multiple providers to enhance coverage and receive diverse assessments, but they face challenges such as limited industry coverage, insufficient data, and a lack of transparency in methodologies. Additionally, the EU market for ESG ratings is unregulated. With increased regulation, the room for companies to exaggerate greenwashing, and capital misallocation could increase.

In response, the European Commission has introduced measures to address concerns about the operations of ESG rating agencies to investors and to promote reliable and comparable ratings. These measures aim to encourage ethical and sustainable investment, aligning with the EU’s greenhouse gas emissions reductions and climate neutrality targets for 2030 and 2050, respectively.

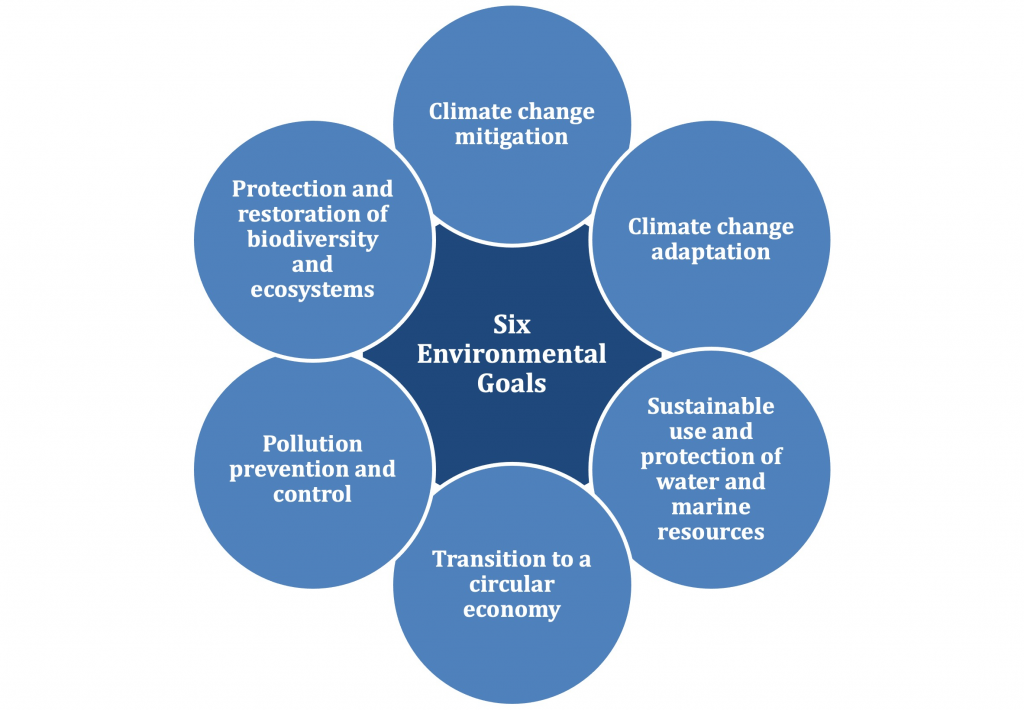

To achieve these targets, significant investment, approximately EUR700bn per year is required, with a focus on private investments aligning with the Sustainable Finance Disclosure Regulation (SFDR) and new criteria being introduced for the EU Taxonomy rules. The EU Taxonomy rules are part of the EU Action Plan on Sustainable Finance and provide a classification system for economic activities that align with the EU’s net zero trajectory for 2050 (Figure 1). They cover six environmental objectives, including climate change mitigation, adaptation, water and marine resource sustainability, circular economy transition, pollution prevention, and biodiversity and ecosystem protection and restoration.

(Figure 1: EU Taxonomy – European Commission)

Early reports show that companies across various sectors are incorporating the EU taxonomy into their transition finance efforts. Transition finance involves using the EU legal framework to guide businesses and the financial industry toward sustainable finance mechanisms and the mitigation of climate and environmental risks. For 2023, results relating to transition finance show encouraging trends among large non-financial companies, with many reporting increasing values of taxonomy alignment, in particular in their capital expenditure.

The importance of advancing the EU Taxonomy and implementing stricter regulation for ESG rating agencies enhances transparency and integrity for EU rating agencies’ methodologies, providing more reliable information for investors and contributing to more effective allocation of capital to sustainable investment activities. Strengthening the usability and coherence of the SFDR demonstrates the EU’s commitment to sustainable finance and responsible investment practices.

While 80% of the market has pledged their support for some sort of legislative intervention, MSCI ESG Research, one of the main rating agencies globally, has stated it maintains a “culture of independence and transparency” in providing ratings and has pushed back on regulations to the sector. They further added on regulatory intervention, “the nascency of the market and the rapid development of services to support the understanding of ESG risks and opportunities means an “industry-supported code of conduct” was more suitable” .

The European Commission’s proposals to address the lack of transparency and align with the SFDR and EU Taxonomy is a step in the right direction. However, little has been proposed to improve standardization across the board. The current situation of varying methodologies and inconsistent ratings leads to confusion among investors allowing cherry-picking of favorable ratings. The Commissions’ draft rules are considered as initial steps towards harmonizing ratings and combating “greenwashing.” However, there are differing opinions on standardizing ESG scoring, ESG still remains very subjective. Therefore, on the standardization front, it is important for regulators to ensure the independence of ratings providers’ methodologies and seek more collective agreement of measurements, methodologies, and disclosures.

Sources

https://ec.europa.eu/commission/presscorner/detail/en/ip_23_3192

https://academic.oup.com/rof/article/26/6/1315/6590670

https://www.iosco.org/library/pubdocs/pdf/IOSCOPD690.pdf

https://www.esma.europa.eu/press-news/esma-news/esma-publishes-results-its-call-evidence-esg-ratings

https://www.esgtoday.com/eu-commission-releases-proposed-regulation-of-esg-ratings-providers/

https://www.leadersarena.global/single-post/esg-ratings-improvements-on-the-horizon

Suivez les performances ESG dans les portefeuilles, créez vos propres cadres ESG et prenez de meilleures décisions commerciales éclairées.

Pour nous contacter, veuillez remplir le formulaire à droite ou nous envoyer directement un email à l'adresse ci-dessous

sales@senecaesg.com7 Straits View, Marina One East Tower, #05-01, Singapour 018936

+(65) 6223 8888

Carrer de la Tapineria, 10

Ciutat Vella, 08002, Barcelona, Spain

+34 612 22 79 06

77 Dunhua South Road, 7F Section 2, Da'an District Taipei City, Taïwan 106414

(+886) 02 2706 2108

Av Jorge Basadre Grohmann 607 San Isidro, Lima, Pérou 15073

(+51) 951 722 377