Interested? Contact us now

In order to contact us please fill the form on the right or directly email us at the address below

sales@senecaesg.com

The Corporate Sustainability Reporting Directive, or CSRD, is a new rule that demands all-inclusive ESG (Environmental, Social and Governance) reporting standards in the EU and sometimes, even outside it. It’s a step-up from the previous Non-Financial Reporting Directive (NFRD) , with added details and a bigger range of businesses that need to follow it. Now, even smaller listed companies and non-EU businesses with important ties to the EU also need to follow these guidelines. The CSRD’s goal is simple: to make it easier for everyone to see and compare how sustainable a business is. It makes sure companies are telling the truth about how they’re doing in ESG aspects.

The Corporate Sustainability Reporting Directive has expanded the range of businesses that need to produce sustainability reports. This is applicable to:

The Corporate Sustainability Reporting Directive was introduced in 2022 but became fully effective at the start of 2024. We have summarized a timeline to help you understand the new requirements better.

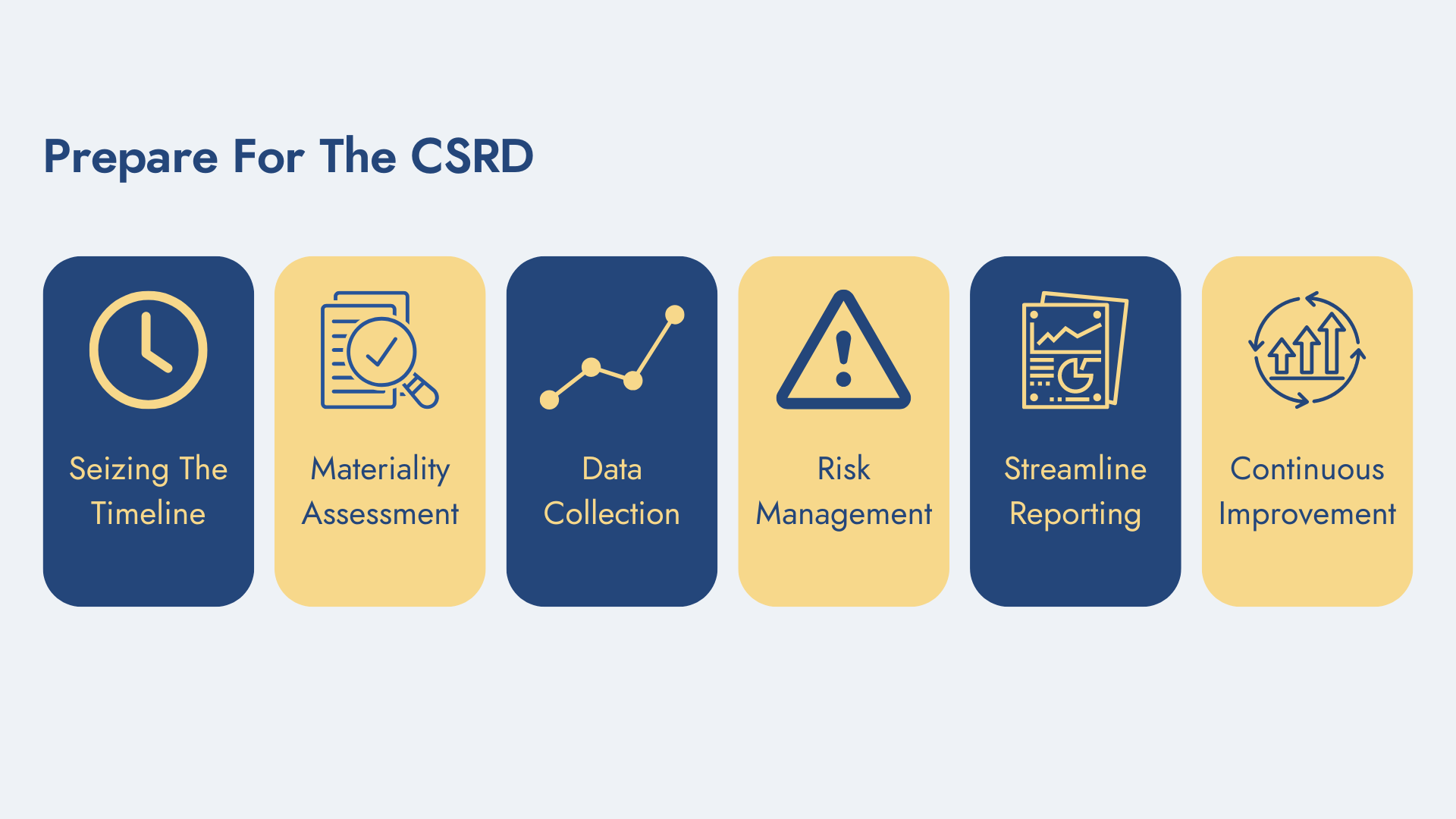

Navigating the complexities of CSRD compliance can seem daunting, but with the right tools and support, you can achieve it faster than you may think. This step-by-step guide offers concise and actionable advice on how to prepare for the CSRD, whether you’re starting from scratch or looking to refine your existing systems. By breaking down the requirements and offering clear directions, the guide is sure to give you the confidence you need to tackle the necessary steps.

Navigating the complexities of CSRD compliance can seem daunting, but with the right tools and support, you can achieve it faster than you may think. This step-by-step guide offers concise and actionable advice on how to prepare for the CSRD, whether you’re starting from scratch or looking to refine your existing systems. By breaking down the requirements and offering clear directions, the guide is sure to give you the confidence you need to tackle the necessary steps.

1/ Seizing The Timeline

Understanding and adhering to the CSRD timeline is crucial for ensuring timely compliance. Start by identifying the specific deadlines that apply to your business category. For large enterprises in the EU, data collection should have begun in January 2024 to prepare for reporting in the following year. It’s essential to maintain a structured schedule to avoid any last-minute rush and ensure the quality of your data.

If your business falls under the category of smaller and medium-sized enterprises, recognize that you have a bit more leeway, with initial data collection starting in January 2026. However, take advantage of this period to build robust systems and processes that will facilitate smoother reporting when the time comes. Remember, even if you have the option to delay reporting, preparing early could give your business a competitive edge and demonstrate a proactive approach to sustainability.

Lastly, for parent companies based outside the EU, start planning for data collection by January 2028. Given the international scope of operations, these companies should pay special attention to aligning their reporting practices with the CSRD requirements to ensure accurate and compliant sustainability reporting in 2029.

2/ Materiality Assessment

When it comes to reporting requirements under the CSRD, disclosure rules vary based on the sustainability topics relevant to each organization. Despite some general requirements and disclosures that all companies must submit, such as ESRS 1 and 2, reporting on other ESRS standards is contingent upon the nature of your business and your exposure to different types of sustainability risk. It is important to keep in mind that virtually all companies reporting under the CSRD will need to report climate change risks and opportunities (ESRS E1). Therefore, it is crucial for organizations to stay informed and up-to-date on the specific reporting requirements that are relevant to their business, in order to ensure a clear and concise report for stakeholders.

Another crucial aspect brought forward by the CSRD is the concept of double materiality. Unlike the traditional materiality that focuses solely on how environmental, social, and governance (ESG) issues affect a company’s financial performance, double materiality requires companies to report not only on how these factors impact their business but also how their business activities impact society and the environment. This dual perspective ensures that the sustainability reports reflect a holistic view of the company’s overall influence, encouraging more responsible and sustainable business practices.

3/ Data Collection

Data collection is a foundational aspect of CSRD compliance, requiring a meticulous approach to gather comprehensive and accurate information across various sustainability metrics. This task involves integrating multiple data sources, standardizing information, and ensuring that the data aligns with the standards. Effective data collection not only involves quantitative measures but also qualitative insights that provide context and depth to sustainability disclosures. Employing advanced data management systems is critical in maintaining the integrity of the data, facilitating real-time monitoring, and simplifying the complex task of sustainability reporting.

With Seneca ESG’s cutting-edge software and tools, businesses can streamline their CSRD compliance journey. Our solutions are designed to simplify the entire data collection process, ensuring thorough integration and ease of use. Featuring advanced analytics, real-time data tracking, and intuitive reporting capabilities, Seneca ESG enables companies to meet regulatory requirements efficiently while also gaining valuable insights into their sustainability performance. Partner with Seneca ESG to transform your reporting practices and showcase your commitment to sustainable development with confidence and precision.  4/ Risk Management

4/ Risk Management

Risk management is a pivotal component in achieving CSRD compliance, focusing on identifying, assessing, and mitigating sustainability-related risks that could impact an organization’s performance.

By implementing a robust risk management framework, businesses can proactively address potential threats and capitalize on arising opportunities, ensuring resilience in the face of environmental, social, and governance challenges. Integrating risk management into your CSRD strategy not only safeguards your business but also enhances stakeholder confidence through a demonstrated commitment to sustainability and responsible governance practices.

The findings from a recent analysis of over 10,000 incidents regarding ESG and stock performance are clear. More than 1,500 corporations were included in the study, and it revealed that controversial actions related to ESG can have a drastic impact on a company’s stock valuation. Within six months of such incidents, companies experienced a decline in valuation ranging from -2% to -5%. This data reinforces the importance of strong ESG practices and the potential negative consequences of falling short.

5/ Streamline Reporting

As companies grapple with new sustainability reporting requirements under the CSRD, some may be pleasantly surprised to find that they are already in compliance with some of the recommendations put forth by the Task Force on Climate-related Financial Disclosures (TCFD). In fact, many organizations may already be making voluntary reports that align with TCFD recommendations or other jurisdiction-specific sustainability disclosure frameworks.

Despite the added work that will inevitably come with complying with the CSRD, it doesn’t have to be done in isolation from other reporting commitments. Instead, companies can look for ways to integrate sustainability reporting into existing frameworks and processes, streamlining workflows and making it easier to stay on top of requirements. So while the new regulations may seem daunting at first, companies that take the time to assess their existing reporting practices and integrate new requirements into their workflows will likely find that complying with the CSRD can be done with minimal disruption.

6/ Continuous Improvement

The final step in aligning with CSRD requirements is committing to continuous improvement. Sustainability is not a static goal but an ongoing journey that requires regular evaluation and enhancement of practices and policies. Companies need to establish mechanisms for continuous monitoring, review, and improvement of their sustainability initiatives. This involves setting actionable sustainability goals, measuring performance against these goals, and making necessary adjustments to strategies based on the insights gained.

Harnessing the power of feedback loops and stakeholder engagement is integral to this process. By actively seeking input from customers, employees, investors, and other stakeholders, companies can identify areas for improvement and ensure their sustainability efforts remain relevant and impactful. Additionally, staying abreast of evolving regulations and industry best practices will help organizations anticipate changes and adapt promptly.

Besides, new rules such as CSRD keep evolving, with shifting schedules and conditions. For this reason, it’s also crucial to constantly stay informed about updates that might impact your company.

Beginning your compliance journey with CSRD can seem daunting, but with the right tools and guidance, it becomes a manageable and even empowering process. Seneca ESG is here to support every step of the way. Our comprehensive solutions enable you to navigate the complexities of sustainability reporting with confidence. By leveraging our expertise and advanced technologies, your business can make informed decisions, ensure accurate compliance, and unlock insights that drive sustainable growth. Empower your organization to meet CSRD requirements effortlessly and effectively with Seneca ESG as your trusted partner. Let us help you take your first steps toward a more sustainable and compliant future.

Sources:

Monitor ESG performance in portfolios, create your own ESG frameworks, and make better informed business decisions.

In order to contact us please fill the form on the right or directly email us at the address below

sales@senecaesg.com7 Straits View, Marina One East Tower, #05-01, Singapore 018936

+(65) 6223 8888

Carrer de la Tapineria, 10

Ciutat Vella, 08002, Barcelona, Spain

+34 612 22 79 06

77 Dunhua South Road, 7F Section 2, Da'an District Taipei City, Taiwan 106414

(+886) 02 2706 2108

Av. Santo Toribio 143,

San Isidro, Lima, Peru, 15073

(+51) 951 722 377