Interested? Contact us now

In order to contact us please fill the form on the right or directly email us at the address below

sales@senecaesg.com

In an important step towards a sustainable economy, this Monday, the European Commission announced its decision to adopt the European Sustainability Reporting Standards (ESRS) for use by all companies subject to the Corporate Sustainability Reporting Directive (CSRD).

The standards encompass environmental, social, and governance issues such as for example climate change mitigation strategy for environment, human rights for social and fair board representation for governance. Designed to support investors with their investment decision-making and comprehension of their sustainability impact, the standards integrate inputs from the recently introduced IFRS S1 and S2 standards from ISSB and the Global Reporting Initiative (GRI). This strong alignment between EU and global standards has the wider objective of reducing redundant reporting by companies.

Effective from 2023 with reporting required from the beginning of 2024, the CSRD is a significant update to the 2014 Non-Financial Reporting Directive (NFRD), extending the number of companies required to provide sustainability disclosures from 12,000 to over 50,000. Although sustainability-focused investor groups welcome the CSRD, there are concerns about the European Commission’s decision to remove the mandatory nature of certain sustainability disclosures, which were originally part of the adopted ESRS.

The ESRS, prepared by the European Financial Reporting Advisory Group (EFRAG), was submitted to the European Commission in November 2022 with modifications to reduce administrative burden and streamline reporting requirements. However, in its proposed version of the final ESRS released in June 2023, the European Commission made significant changes. Notably, it suggested subjecting all disclosure requirements, except for general disclosures, to materiality assessments. This allows companies to focus their reporting on sustainability factors they deem crucial to their businesses. Additionally, the changes involve phasing in certain reporting requirements and specific disclosures for smaller companies during their initial year of applying the standards.

Investment and finance groups expressed concerns with the EU Commission’s amendments, citing potential impacts on their ability to obtain essential sustainability-related information for investment decisions. They also fear reduced compliance with their own reporting requirements, including those under the EU’s Sustainable Finance Disclosure Regulation (SFDR).

To relieve concerns from investors, the European Commission has published a detailed Q&A following the adoption of the ESRS which is designed to inform investors the reasoning behind the decision taken to adopt the ESRS.

Why is the Commission adopting ESRS?

Under EU law, all large companies, and listed companies (excluding listed micro-enterprises) are required to disclose information about social and environmental risks, opportunities, and their impact on people and the environment. However, the current sustainability reporting is inadequate and lacks important information. This poses challenges for investors and stakeholders to assess companies’ sustainability performance effectively. Insufficient reporting therefore can lead to a lack of understanding of companies’ sustainability risks, affecting the credibility of the green investment market.

To address this, the European Commission’s decision to adopt the European Sustainability Reporting Standards (ESRS) as common standards is to enhance the communication and management of sustainability performance. These standards will be compulsory for companies obligated to report sustainability information under the Accounting Directive, ensuring consistent and reliable reporting across the EU and reducing reporting costs in the long term. The overarching aim will be to foster a culture of greater public accountability through high-quality and reliable ESG reporting by companies.

What will companies have to report?

The ESRS (European Sustainability Reporting Standards) have been developed following the provisions of the Accounting Directive, amended by the CSRD. As required by the Accounting Directive, the ESRS takes a double materiality approach. Mandatory reporting on company impacts in relation to the environment and people as well as how social and environmental issues create financial risks and opportunities for the company must also be included.

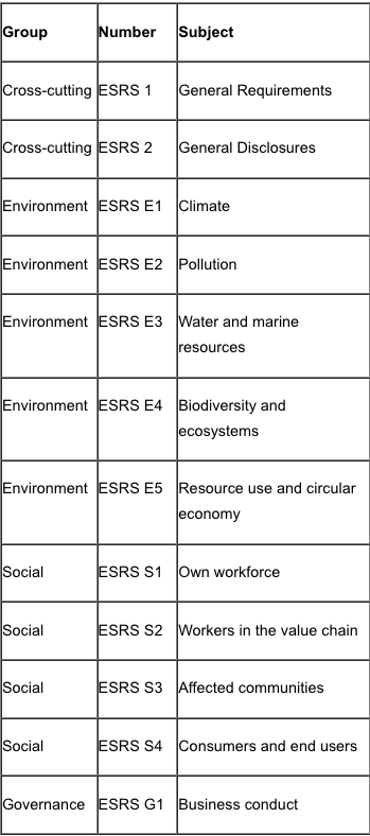

(Figure 1 – European Commission: 12 ESRS in line with EFRAG’s proposal)

In summary, ESRS 1 sets general principles for reporting, while ESRS 2 mandates essential disclosures for all companies under CSRD. Other standards have disclosure requirements subject to materiality, meaning companies must report relevant information based on a materiality assessment. Regarding Materiality assessments, they are externally assured and require necessary sustainability information is disclosed. For the application of Climate Change, if a company decides climate change isn’t material, it must provide a detailed explanation due to its significant environmental impact on the economy.

Alignment with other EU legislation

Specifically, the ESRS contains datapoints required for reporting under the Sustainable Finance Disclosure Regulation (SFDR), the Benchmark Regulation (BMR), and the Capital Requirements Regulation (CRR). If a company determines that a data point from SFDR, BMR, or CRR is not material, they must explicitly state it as “not material” in their reporting instead of just providing no information. The company will also need to include a table with all such non-material data points and their location in their sustainability statement. These provisions will ultimately help financial market participants, benchmark administrators, and financial institutions comply with their respective disclosure obligations under SFDR, BMR, and CRR.

With ESRS coming into effective from 2024, companies seeking further guidance on the application can rely on EFRAG’s expertise and credibility in helping shape the ESRS. In support EFRAG will also publish technical guidance, with a focus on materiality assessment and reporting regarding value chains. Moreover, EFRAG will provide a portal for technical questions, and the Commission may also offer guidance on legal interpretations. Additionally, EFRAG will collaborate with ISSB and the recent release of their standards to optimize the interoperability of overlapping ESRS and ISSB standards for companies aiming to comply with both.

Sources

Monitor ESG performance in portfolios, create your own ESG frameworks, and make better informed business decisions.

In order to contact us please fill the form on the right or directly email us at the address below

sales@senecaesg.com7 Straits View, Marina One East Tower, #05-01, Singapore 018936

+(65) 6223 8888

Carrer de la Tapineria, 10

Ciutat Vella, 08002, Barcelona, Spain

+34 612 22 79 06

77 Dunhua South Road, 7F Section 2, Da'an District Taipei City, Taiwan 106414

(+886) 02 2706 2108

Av. Santo Toribio 143,

San Isidro, Lima, Peru, 15073

(+51) 951 722 377