Interested? Contact us now

In order to contact us please fill the form on the right or directly email us at the address below

sales@senecaesg.com

The Intergovernmental Panel on Climate Change (IPCC), the world’s leading authority on climate science, released the “Working Group II: Impacts, Adaptation and Vulnerability Report” (WG2 report) on February 27, 2022, as the second part of its sixth assessment report (AR6). The 3675-page report summarized the latest science on the impacts of climate change on communities and ecosystems, our efforts to adapt to these impacts, and our vulnerability to future impacts.

The first part of the AR6 (WG1 report) was released in August 2021 to summarize the latest scientific interpretation of what causes climate change. A third and final part of the AR6 (WG3 report) will work to address the mitigation of climate change and is expected to be published in March or April of this year.

Bleak Realities from the IPCC WG2 Report

With the greenhouse gases already emitted to the atmosphere, the world is locked into even worse impacts of climate change in the near term even if it decarbonizes rapidly. Moreover, given the current imbalance of development, the world’s poorest and most vulnerable communities will bear the brunt of climate impacts. UN secretary-general Antonio Guterres has gone as far as calling the WG2 report “an atlas of human suffering and a damning indictment of fake climate leadership.”

The WG2 report highlighted several bleak projections and observations regarding the effects of climate change:

The WG2 report also highlighted the transboundary risks of climate change. Climate change impacts not only allude to the physical impacts of climate and weather events on neighboring countries but also stressors and disruptions to trade and finance networks. For example, disruptions in food production in one country or the product’s maritime routes may lead to food insecurity for another country, who imports most of its food source from that country, despite their physical distance. As the planet continues to heat up, no country or industry could be exempt from its implications.

Adaptation Finance: A Long Way to Go

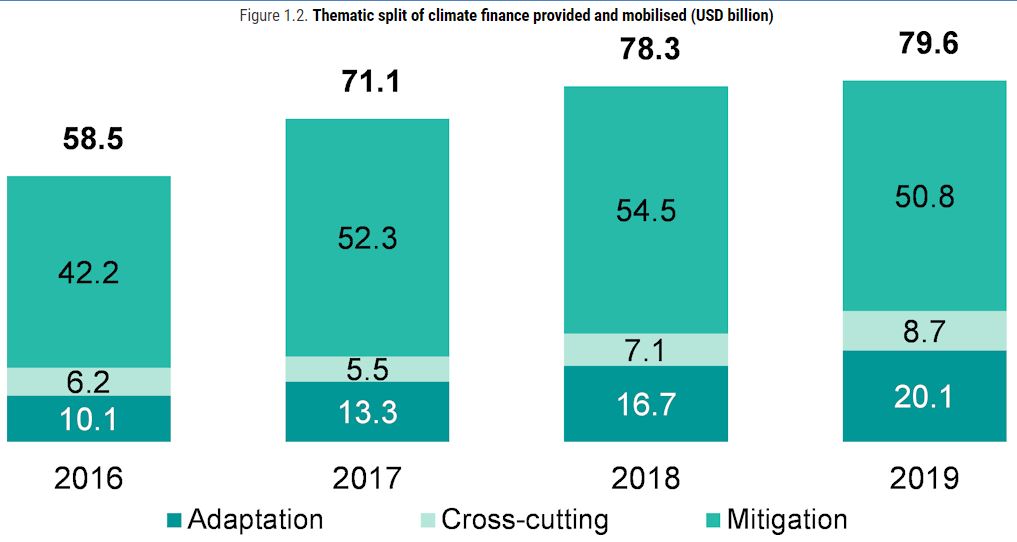

The WG2 report warns that there has been a continued heavy imbalance between current levels of adaptation and levels needed to respond to impacts and reduce climate risks. Such gaps are partially driven by widening disparities between the estimated costs of adaptation and documented finance allocated to adaptation. Currently, the overwhelming majority of global climate finance has been dedicated to mitigation efforts. In a report, the OECD aggregated the amount of climate finance provided and mobilized by developed countries up to 2019, which showed that developed countries are yet to reach their 2009 pledge of channeling USD100bn per year towards climate finance for less developed countries. Moreover, of the amount provided, less than one-third went towards adaptation efforts.

Source: OECD

Effective adaptation measures require a nuanced and tailored approach for the specific location and community it attempts to help. As a result, it receives much lower levels of investments than mitigation efforts, which may deploy clean technologies using a blanket approach. The tech-centered nature of many mitigation projects also appeals to investors due to predictable returns, while adaptation projects are centered around the prevention of potential losses and may involve nature-based approaches. The challenge is to highlight the economic sense of adaptation and engage more investors on the other side of climate finance.

The Economic Sense of Adaptation

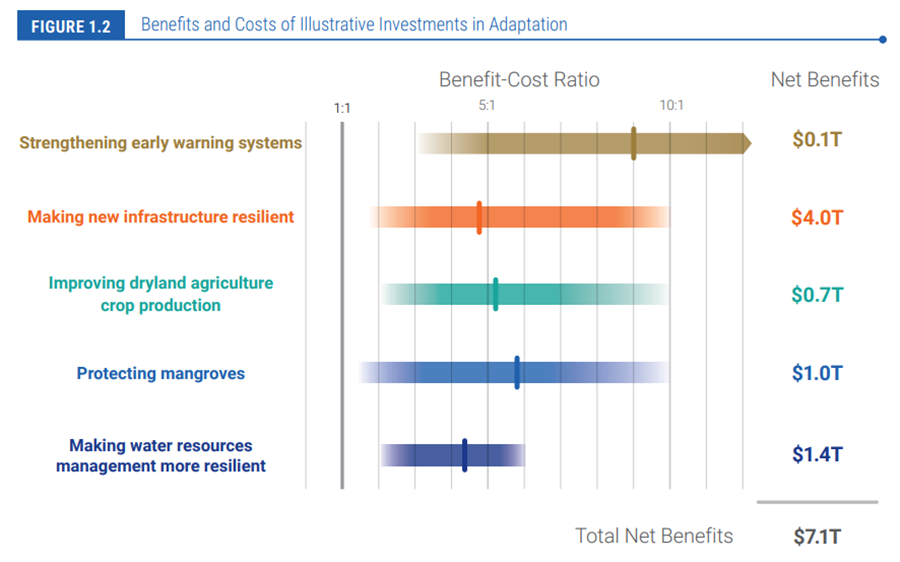

Even though adaptation finance demands more creative solutions from decision-makers, investing in adaptation is not only necessary but also economically beneficial. According to analysis from the Global Commission on Adaptation, every USD1 invested in adaptation generates a return between USD2 and USD10, since recovery and rebuilding typically cost much more. If the world fails to seize these high-return investments, it may lose trillions of dollars in potential growth and prosperity. The graph below illustrates the benefit-cost ratio of adaptation investments from 2020 to 2030, assuming USD1.8tr of investments in five areas of work. The projected result is USD7.1tr in total net benefits.

Source: Global Commission on Adaptation

Such economic gains are derived from three main benefits. The first is avoided losses, such as the financial losses for coastal assets due to storm surges and sea-level rise. This is typically the most common motivation for investment in resilience. The second benefit is the reduction of risks, the increase of productivity, and innovation through adaptation needs. For example, retrofitting buildings with outdated weatherproofing could not only lower energy consumption, thereby reducing the risk of outages, but also enhance the productivity of workers by improving their physical wellbeing at work. Lastly, many adaptation actions can generate significant additional economic, social, and environmental benefits. For instance, the restoration of natural land in urban areas not only helps mitigate flash floods but also improves biodiversity and human health. These benefits accrue on an ongoing basis.

Unlocking Private Finance for Adaptation

According to Climate Policy Initiative, from 2019 to 2020, 98% of the world’s adaptation finance came from public actors, such as multilateral development banks and national development banks. Private capital for adaptation occupies a much smaller share and typically comes from corporations of all sizes, institutional investors, and even households. To galvanize private capital for climate adaptation, the Climate Policy Initiative suggested the following three actions:

Sources:

https://chinadialogue.net/en/climate/ipcc-report-is-blueprint-for-a-future-on-the-planet/

https://www.sei.org/perspectives/ipcc-report-for-adaptation/

https://report.ipcc.ch/ar6wg2/pdf/IPCC_AR6_WGII_SummaryForPolicymakers.pdf

https://files.wri.org/s3fs-public/uploads/GlobalCommission_Report_FINAL.pdf

https://www.climatepolicyinitiative.org/unlocking-private-sector-adaptation-finance/

Monitor ESG performance in portfolios, create your own ESG frameworks, and make better informed business decisions.

In order to contact us please fill the form on the right or directly email us at the address below

sales@senecaesg.com7 Straits View, Marina One East Tower, #05-01, Singapore 018936

+(65) 6223 8888

Carrer de la Tapineria, 10

Ciutat Vella, 08002, Barcelona, Spain

+34 612 22 79 06

77 Dunhua South Road, 7F Section 2, Da'an District Taipei City, Taiwan 106414

(+886) 02 2706 2108

Av. Santo Toribio 143,

San Isidro, Lima, Peru, 15073

(+51) 951 722 377